This article is Part 1 of a series on evaluating the ways to add Portfolio Insurance if you are anticipating a market correction or market decline.

Most of us are probably in more Bullish positions, based on the last 12 months performance of the market. Every week new highs are being hit, and bullish stock and option traders have been doing well.

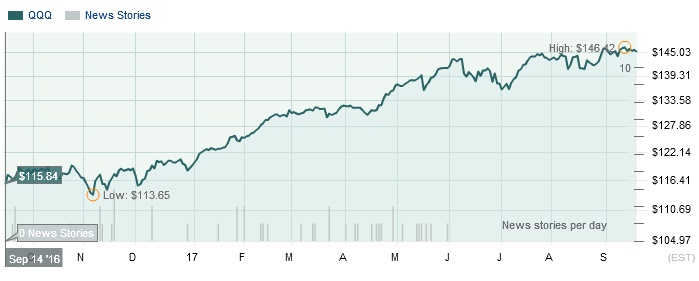

Over the last 12 months, we have seen SPX (S&P 500 index) and SPY (S&P 500 ETF) gain over 17% (SEP 13th, 2016, SPY closed at $213.23 and is currently around $250.00).

During that same time period, NDX (NASDAQ 100 index) and QQQ move up 26% (SEP 14th, 2016, QQQ at $115.85 to about $146.00).

Sure, there were small hiccups here and there along the way, but the extended growth has led to many pundits, gurus and other stock prognosticators warning of a downturn and correction.

So the question many of you have been posing to us here at PowerOptions is:

“What is the best way to protect my portfolio against a -X% decline in the market?”

There are many ways to potentially hedge an investment portfolio, but this question is missing a few key factors. The most important of which is: ‘How much do you want to protect?’

A Look at the Most Basic Example.

Let’s say we have a $1,000,000 account, and for the sake of argument let’s say 80% of that is invested in SPY. This is not an advisable allocation of funds, but it would have an unrealized gain of 17% as we just saw.

So, $800,000 is invested in SPY. You are expecting a -10% market downturn, or a loss of -$80,000 on your investment. How can you protect against a -10% downturn?

Well, how much do you want to protect? This is one of the points that is missing from the initial question.

If you are comfortable only risking -5% of invested capital in a -10% decline, you could simply set a stop order (in this basic scenario) to close your shares of SPY if they drop -5% from the current value.

With SPY at $250.00, we would set a stop at $237.50, -$12.50 from the current price.

As long as that price is hit during the trading day, you would close out your position and only have a -5% loss from the current value – now a realized gain of $24.30 per share, or 11.8% if you had bought in and held from last year.

BUT! We all know the dangers of stop orders. It is really just a market order that tells your broker: Close my position if the stock / security is anywhere below that price at any time.

It is unlikely to happen with SPY, QQQ or a broad market ETF, but IF SPY gapped down -15% overnight – you don’t get to close the position at $237.50. Your order is triggered and you are closed out at whatever the market is offering…in this case, $212.50. You are now at a small loss on the total position from your original cost of $213.23. That is not what we want to see.

Again, that is not likely to happen in this case. But, what if you wanted to stay in the position and not be automatically closed out – and at the same time protect against an expected decline?

You would need an instrument, and the corresponding number of shares (or option contracts), that would gain $40,000 if you expected your portfolio to drop -$80,0000.

Common ways for Stock Traders to Insure a Portfolio:

We already talked about a Stop, which also includes a Trailing Stop. That is common protection #1.

But if we want control of our position and not leave it subject to a set number or the risk of the stop being violated, we would look at a different approach.

SPY is right around $250.00. If we invested $800,000 (or 80% of our portfolio) into shares of SPY we would purchase 3,200 shares.

And…yes, let’s throw out the logic that if we were expecting a -10% downturn in the market we would not be buying SPY today. Of course we wouldn’t be doing this. But, let’s work the numbers for a proper hedge…

What are the obvious hedges?

- Set a Stop at -5% ($237.50) or a Trailing Stop. We just covered the pros and cons of a simple stop. It’s free, yes, but can be violated.

- Sell out now, stay in Cash. This is always an advisable approach if you are considering a market downturn and you have hit your target for profit. Close out your bullish securities for gains or small losses, stay in cash and wait it out. But, we are looking for better solutions here, not the obvious.

- Buy shares of the inverse ETF which will gain as the market falls. Inverse ETFs will move counter market, allowing investors to potentially hedge a portfolio.

ProShares Short S&P 500 (SH), an inverse ETF against SPY.

SH is currently trading at $32.45. If SPY declines -10%, SH would rise +10%, or roughly $3.25 to $35.70.

We need a $40,000 gain to counter the -$80,000 loss:

($40,000 needed / $3.25 gain per share (SH)) = 12,307

To counter half of the $80,000 loss on SPY we would need to purchase 12,307 shares of SH. This would be a total cost of $399,362.15.

Well, that doesn’t work. First, we only have $200,000 of free capital in our $1,000,000 account. Second, if the decline does not happen and the stock moves up, we are losing money on the $400,000 investment. Third, it is just not that efficient.

| Security | # of Shares | Price / Share | Investment | Value -10% decline | Gain / Loss |

| SPY | 3200 | $250.00 | $800,000.00 | $720,000.00 | -$80,000.00 |

| SH (hedge) | 12307 | $32.45 | $399,362.15 | $439,359.90 | +$39,997.75 |

With this hedge we would have cut the loss in half to only -$40,000, or only -5% of our invested capital. This also represents only a -4% loss of the entire portfolio value. BUT, we would have to trade this on margin as we did not have the capital required to purchase that many shares of the inverse ETF.

We would want to use some kind of leverage to better hedge the position.

There are 2X and 3X Bear ETFs for SPY:

Pro Shares UltraShort S&P 500 (2X) ETF – SDS currently at $47.53

Direxion Daily S&P500 Bear 3X ETF – SPXS currently at $37.37

4. Buy shares of Leveraged, Inverse ETFs to hedge the position.

Percentage wise these securities will move twice or three times the amount of the movement in SPY.

A -10% decrease in SPY should result in a +20% increase in SDS, or a 30% increase in SPXS. So how many shares would be needed to counter half of our -$80,000 loss on investment?

With a -10% decrease, SDS should gain +20%, or +$9.50 to $57.03. To gain $40,000, we would need to purchase 4,210 shares of SDS ($40,000 needed / $9.50 gain per share = 4,210):

| Security | # of Shares | Price / Share | Investment | Value -10% decline

(SPY at $225.00; SDS at $57.03) |

Gain / Loss |

| SPY | 3200 | $250.00 | $800,000.00 | $720,000.00 | -$80,000.00 |

| SDS (2X Bear) | 4210 | $47.53 | $200,101.30 | $240,096.30 | +$39,997.75 |

So this is an easier pill to swallow, but it would still require an investment of just over $200,000, what is left in the portfolio, to cut the loss on SPY by 50%.

What about using more leverage with the 3X Bear ETF? SPXS should rise +30% with the decline. This would be a gain of $11.21 to $48.58.

| Security | # of Shares | Price / Share | Investment | Value -10% decline

(SPY at $225.00; SPXS at $48.58) |

Gain / Loss |

| SPY | 3200 | $250.00 | $800,000.00 | $720,000.00 | -$80,000.00 |

| SPXS (3X Bear) | 3568 | $37.37 | $133,336.16 | $173,333.44 | +$39,997.28 |

Now at least we can afford to purchase the number of shares required to lower our loss to only -5%, or -$40,000. But, aren’t there better methods of leverage? Hey, this is why we use options!

Option 5: Buy Puts directly on SPY.

Put options are extremely useful for insuring or protecting stock directly, or a portfolio. As the stock or market falls, the put options gain in value. There is a cost, but options give us leverage for both bullish gains, bearish gains, or protecting Bullish or Bearish portfolios.

If I wanted to hedge a position to counter 50% of the expected move, I might look at an At-the-Money put (close to the current stock price) with a Delta of 0.50 (would gain $0.50 for every -$1.00 drop in the stock price).

Unlike purchasing shares of an inverse and leveraged ETF as a hedge, the put option has a defined expiration date.

If I expected a -10% decline in the markets over the next two weeks, I may look to standard October expiration, 2017 (20-OCT – 30 days out in time):

Hedge: Purchase 20-OCT 250 strike puts at $1.95

One put contract represents 100 shares of the underlying security. The listed price of $1.95 / contract would actually cost $195.00 to purchase 1 contract.

If SPY fell to $225, say on October 13th, 2017 – the put option would be trading at close to Intrinsic Value (the amount that the put option is In-the-Money). We would expect the put option to be trading at a value of at least $25.00 per contract. So, how many put contracts would we need to buy to counter half of the projected $80,000 loss?

Original cost per contract = $1.95 ($195.00)

Minimum Value if SPY is at $225.00 = $25.00 / contract ($2,500)

Gain on Hedge = 25.00-1.95 = $23.05 / contract ($2,305)

$40,000 needed / $2,305 profit per hedge = 17.3 contracts (let’s just call it 18)

Hedge Action: Buy 18 contracts 20-OCT 250 put @ $1.95 / contract

Total Cost = (18 * 1.95) * 100 = $3,510.00

| Security | # of Shares / Contracts | Price / Share

Price / Contract |

Investment | Value -10% decline

(SPY at $225.00) |

Gain / Loss |

| SPY | 3200 | $250.00 | $800,000.00 | $720,000.00 | -$80,000.00 |

| 20-OCT 250 Put | 18 | $1.95 | $3,510 | $45,000.00 | +$41,490.00 |

This structure creates what is called a Married Put or Protected Put position. It is not done at a 1:1 ratio (32 contracts against the 3200 shares of SPY) which is the preferred structure, but it does satisfy our needs:

- By only putting up 0.35% of our total portfolio value, or 1.7% of our remaining $200,000 in cash, we have hedged a potential -10% portfolio loss to only -5%.

- WE control the outcome of the position. We can not be closed out (unless we hold the put to expiration and make no adjustments) or assigned. We bought the put, we control what happens next.

- This is better protection against a sudden -10% market decline, over a -5% Stop Order or Trailing Stop that could be violated.

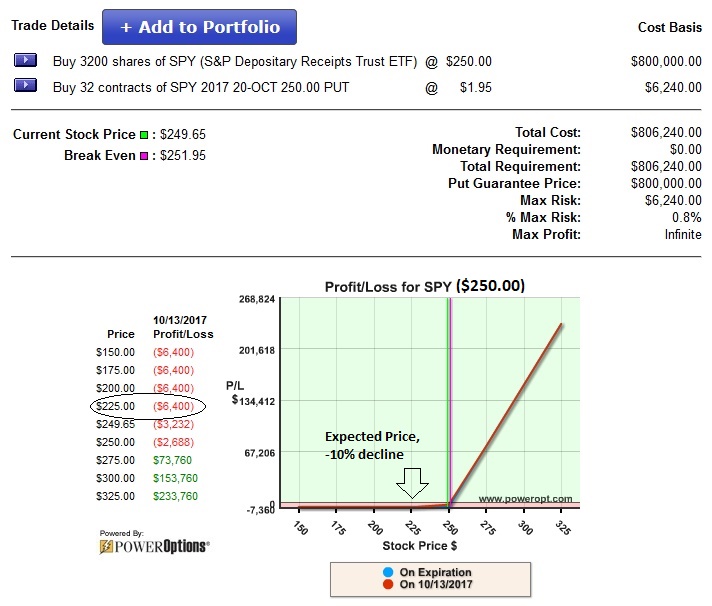

But, there are negatives to this approach. If SPY fell further than -10%, we could realize larger losses as we only protected 1,800 shares of our 3,200 share investment. For a little more capital we could insure all 3,200 shares. Let’s look at the ‘5-line setup’ of a full Married Put / Protected Put:

Own 3,200 shares of SPY at $250.00 ($800,000 total)

Buy 32 cont. 20-OCT 250 puts at $1.95 (6,240.00 total)

Total Investment = $251.95 per share ($806,240.00 total)

Guaranteed Exit = -$250.00 per share ($800,000 guaranteed)

Maximum Risk = $ 1.95 per share, or 0.8% ($6,240.00)

Although this is more expensive than hedging part of the full trade:

- We only use 3.1% of our remaining $200,000 capital, or 0.62% of our total portfolio value…AND the Max. Risk in any decline scenario is only 0.8% of our capital invested, even if the decline is larger than we thought.

- We still control the outcome of the position, and can not be closed out early or assigned.

- We have covered the full 3,200 share block with only a small percentage of our account value. We could even buy more for a higher cost and actually PROFIT to the Downside, as well!

- And of course, this example relates to other size portfolios, not just a $1,000,000 account. You could apply this to a $100,000 if you were 80% invested, a $10,000 account or even a $1,000 account.

This is a much more cost effective and efficient way to protect against an expected market decline.

What are the risks? If the decline DOES NOT happen during your expected time frame you may lose the cost of insurance, $6,240, as the put would expire worthless. However, if the market continues up, you have not capped the upside gain and can still realize more profit. Which brings us to the final topic on this basic example…

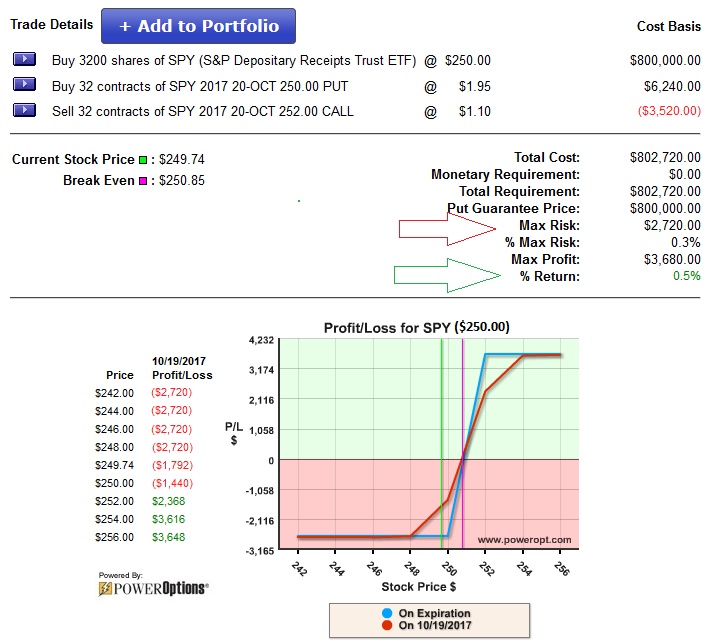

Can’t I use other transactions to pay for the insurance?

We all know that trading options carries risks, just like any form of investing. Many options traders prefer to Sell Premium rather then Buy Premium. However, selling premium against a security only offers a small amount of protection, compared to buying insurance.

We could lower the cost of the insurance by selling a call against the security in this scenario. If we sold the 20-OCT 252 strike call, we could generate $1.10 in premium, cutting the cost of the insurance in half. This would create a Standard Collar position.

However, selling a call obligates us to deliver our shares at the strike ($252.00) if the stock is trading above that price. Although we cut the risk in half, we also limit the gains if we are wrong and the market continues up in price, as you can see from the Profit / Loss chart.

By selling the 20-OCT 252 strike call we lower the risk to only 0.3% of our invested capital. However, we cap the upside to only 0.5% gain, or $3,680.00 of the +$800,000 invested. This might not be a concern, as we are expecting a -10% decline in the market…but it is something to consider.

What have we covered so far?

We have looked at some of the basic ways a stock investor might consider insuring against an expected decline. Let’s rec

1. Set a -5% Stop or Trailing Stop

Pros: Free, Easy to Use

Cons: Can be violated, you do not control the outcome

2. Sell out now, Stay in Cash

Pros: Safe, effective, keep your capital

Cons: Miss further upside if decline does not happen

3. Buy the direct Inverse ETF

Pros: Simple stock purchase, don’t need options

Cons: Not cost effective at all!

4. Buy a 2X or 3X Inverse ETF

Pros: Simple purchase, don’t need options, better than standard inverse

Cons: Still not cost effective

5. Buy a Put to Insure against the decline

Pros: Leverage, lower cost, can protect the expected decline or 1:1

Cons: Requires Cost unlike a Stop…but you get what you pay for – peace of mind!

6. Create a Collar to cut down the cost of insurance

Pros: Generate premium, cut insurance cost and risk in half

Cons: Caps the upside if market continues up and no decline

But there are so many different ways to create Portfolio Insurance against a market decline. But first, we want to take a look at the proper strike selection to insure this example and using Put options to insure an actual stock portfolio!

Here is a preview of what to expect in the next few days:

Part 2: Proper ETF/Index put selection to Hedge a Real Stock Portfolio

Part 3: Other option Hedges for Stock and Options Portfolios

Part 4: Real Examples of Potential Hedges from the Past and Looking Forward

Allan

Hi Mike,

This is very timely as I have been contemplating just this type of strategy. Thanks for the great info and looking forward to the remaining portions.

Michael Chupka Post author

Hello Allan, I am glad to hear that you found the information useful. We should have another updated today, and more coming this week!

Ray

Thanks this is really helpful for those of us looking for a little peace of mind.

Michael Chupka Post author

Hello Ray, you are welcome. I will have more information for you today, and during this week.

David H Holan

Michael,

How would you manage the married put to minimize risk and maximize profit if the position keeps going up? Please continue with the same strategy.

Michael Chupka Post author

Hello David, If SPY continued up after the insurance was in place, I would likely use one of the income methods discussed in The Blueprint applying the Radioactive Trading techniques. Income Method #6, a Bear Call spread in the structure of a Married Put is a great way to generate income but not cap the gains as one does with simply selling a call (creating a Collar).

I could also adjust the put option if SPY continues up to lower any risk, although with such a short term position – that was based on hedging against a downturn not profiting in an uptrend – I might just consider letting the stock ride and using the Bear Spread (in the context of a Married Put / Protective Put) to leave the upside open. You will see more tomorrow on selecting the right strike price and further details.

David Swartz

The section on buying shares of leveraged inverse ETFs to hedge is not very accurate. It is incorrect to suggest that SDS or SPXS will move in predictable ways over time. These ETFs track the inverse of the S&P 500 for single days only. SPXS would not probably not increase exactly 30% if the S&P 500 fell 10%.